January 08, 2020

Should I Pay Off Debt or Invest?

Dentists are no strangers to debt. From accumulating student loans in dental school to incurring debt to purchase your practice, equipment and office, dentists will spend their entire professional careers dealing with loans.

It comes as no surprise, then, that the first question we often hear from dentists is, “Should I invest now or use those dollars to pay off my debt first?”

Let’s acknowledge up front that owing money to someone else can be emotionally upsetting. So it follows that paying off a debt results in a feeling of relief and freedom. Thus, listeners to The Dave Ramsey Show call in to excitedly exclaim, “I’m debt free!”

But, setting emotions aside, I believe the answer to this question isn’t an either/or proposition. I believe there are legitimate and constructive ways to use debt and at the same time create wealth. By its very nature, debt affords a dentist time to develop and grow a business, purchase a home, or gain knowledge (i.e., attend dental school). Without loans, most of us would never be able to pay full price up front for some important things.

The following example, a hypothetical illustration, attempts to offer some insight on how to prioritize debt repayment versus investing.

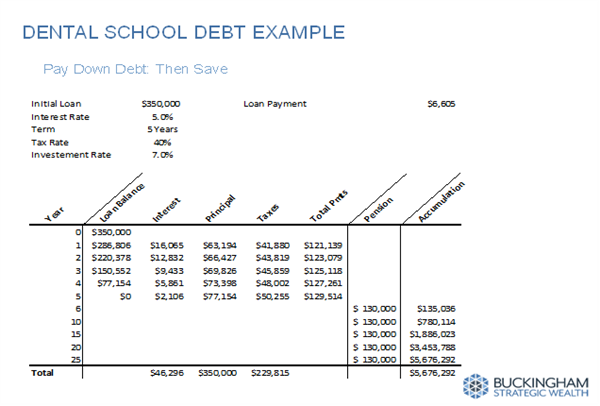

In Exhibit 1, a dentist with $350,000 of student debt initially forgoes any savings by paying off her debt (a little less than $130,000 annually) in five years. For the remaining 20 years of her career, she saves $130,000 annually in tax-deferred pension plans (i.e., 401(k), cash balance defined benefit plan). Our dentist accumulates $5.7 million at retirement.

Exhibit 1

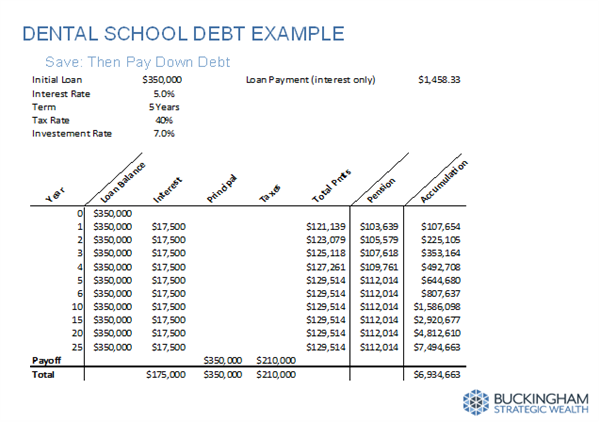

Compare this to Exhibit 2, where our dentist instead pays only interest on her student debt ($17,500 annually) and invests the remaining $103,000 to $112,000 each year in the same tax-deferred savings vehicles. At the end of 25 years, a portion of the accumulated retirement savings is used to pay off the student debt.

Exhibit 2

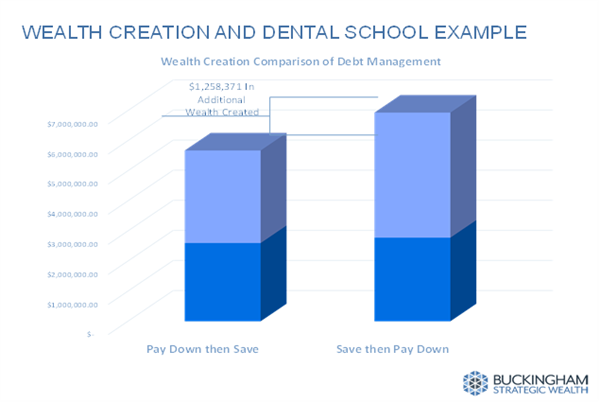

In this case, our dentist accumulates $6.9 million, which is $1.2 million more than with the first strategy.

Exhibit 3

I realize that paying only interest on student debt is unrealistic. But this example does illustrate the opportunity dentists have to build significant wealth over time by prioritizing savings over accelerated debt repayment. Put another way, taking advantage of the time provided by a reasonable debt repayment plan gives you the opportunity to start investing early and longer enjoy the fruits of compound growth.

Still have questions? Please reach out to any of Buckingham’s Practice Integration Advisors. We are here to help! Also, stay tuned for our next post, from my colleague, Katie Collins, who provides some thoughts on how best to deal with student loans.

By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party Web sites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them.

The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth®. This article is for general information only and is not intended to serve as specific financial, accounting or tax advice.

© 2019, Buckingham Strategic Wealth®

Category

Business OwnershipContent Topics

Stay Connected With Buckingham

Want more resources like this? Click here to receive financial insights, articles, videos and webinar invitations.